30.6 Change in a reporting entity and common control transactions

30.8 Reclassifications (accounting changes)

Favorited Content

- 30.7 Correction of an error

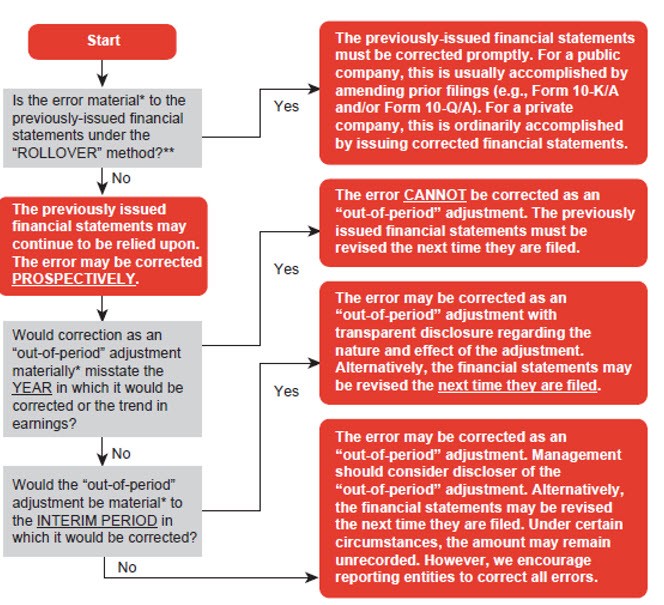

- The “rollover” method assesses income statement errors based on the amount by which the income statement for the period is misstated—including the reversing effect of any prior period errors. Identified misstatements in the previous period that were not corrected need to be considered to determine any “carryover effects.”

- The “iron curtain” method assesses income statement errors based on the amount by which the income statement would be misstated if the accumulated amount of the errors that remain in the balance sheet at the end of the period were corrected through the income statement during that period.

30.7.1 Restatements (error corrections)

- Filing an Item 4.02 Form 8-K to indicate that the previously issued financial statements should no longer be relied upon. The reporting entity should consult with its counsel to determine the appropriate steps and timing for providing notice that the financial statements should no longer be relied upon.

- Amending prior filings (e.g., filing Form 10-K /A and/or Form 10-Q /A, or, in limited circumstances, a Form 10-K when filing of the subsequent year’s Form 10-K is imminent)

- For a private company, the correction of a material misstatement is ordinarily accomplished by the company issuing corrected financial statements that indicate that they have been restated and include its auditor’s reissued audit report. Alternatively, it is permissible to reflect the restatement in the soon-to-be issued comparative financial statements. When the restatement is to be reflected in the soon-to-be issued comparative financial statements, the financial statements and auditor’s report would indicate that the prior periods have been restated. Users of the previously issued financial statements also must be notified that they should no longer rely on those financial statements.

Excerpt from ASC 250-10-45-23

- The cumulative effect of the error on periods prior to those presented shall be reflected in the carrying amounts of assets and liabilities as of the beginning of the first period presented.

- An offsetting adjustment, if any, shall be made to the opening balance of retained earnings (or other appropriate components of equity or net assets in the statement of financial position) for that period.

- Financial statements for each individual prior period presented shall be adjusted to reflect correction of the period-specific effects of the error.

ASC 250-10-50-7

When financial statements are restated to correct an error, the entity shall disclose that its previously issued financial statements have been restated, along with a description of the nature of the error. The entity also shall disclose both of the following: a. The effect of the correction on each financial statement line item and any per-share amounts affected for each prior period presented b. The cumulative effect of the change on retained earnings or other appropriate components of equity or net assets in the statement of financial position, as of the beginning of the earliest period presented.

ASC 250-10-50-8

When prior period adjustments are recorded, the resulting effects (both gross and net of applicable income tax) on the net income of prior periods shall be disclosed in the annual report for the year in which the adjustments are made and in interim reports issued during that year after the date of recording the adjustments.

ASC 250-10-50-9

When financial statements for a single period only are presented, this disclosure shall indicate the effects of such restatement on the balance of retained earnings at the beginning of the period and on the net income of the immediately preceding period. When financial statements for more than one period are presented, which is ordinarily the preferable procedure, the disclosure shall include the effects for each of the periods included in the statements. (See Section 205-10-45 and paragraph 205-10-50-1 .) Such disclosures shall include the amounts of income tax applicable to the prior period adjustments. Disclosure of restatements in annual reports issued after the first such post-revision disclosure would ordinarily not be required.

30.7.2 Revisions and out-of-period adjustments (error corrections)

- Recording an out-of-period adjustment, with appropriate disclosure, in the current period, if such correction does not create a material misstatement in the current year

- Revising the prior period financial statements the next time they are presented

- FSP Corp’s reported income in each of the years 20X1 through 20X4 was $1,000.

- FSP Corp projects its 20X5 income will be $1,000.

- FSP Corp may correct the errors as an “out-of-period” adjustment in its first quarter 20X5 interim financial statements if the correction would not result in a material misstatement of the estimated fiscal year 20X5 earnings ($1,000) or to the trend in earnings. This is true even if the “out-of-period” adjustment is material to the first quarter 20X5 interim financial statements. If the “out-of-period” adjustment is material to the first quarter 20X5 interim financial statements (but not material with respect to the estimated income for the full fiscal year 20X5 or to the trend of earnings), then the correction may still be recorded in the first quarter, but should be separately disclosed (in accordance with ASC 250-10-45-27 ).

- If FSP Corp cannot correct the errors as an “out-of-period” adjustment without causing a material misstatement of the estimated fiscal year 20X5 earnings ($1,000) or to the trend in earnings, then the errors must be corrected by revising the previously issued financial statements the next time they are filed (e.g., for comparative purposes). For instance, the quarterly financial statements for the first quarter of 20X4 and the December 31, 20X4 balance sheet presented in FSP Corp’s March 31, 20X5 Form 10-Q should be revised to correct the error. The revised financial statements should include transparent disclosure regarding the nature and amount of each error being corrected. The disclosure should provide insight into how the errors affect all relevant periods (including those that will be revised in subsequent filings).

30.7.3 Misclassifications (error corrections)

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

- Add to favorites

Search within this section

Select a section below and enter your search term, or to search all click Financial statement presentation

This content is copyright protected. It is for your own use only - do not redistribute. These materials were downloaded from PwC's Viewpoint (viewpoint.pwc.com) under license.

Your recent searches

Suggested terms, suggested guidance.

- current step: 1. Warning 2

- 2. Warning 2

- 3. Warning 2

{{isCompleteProfile ? "Setup your profile before Sign In" : "Profile"}}

{{editProfile.email}}

Preferences

You can set the default content filter to expand search across territories.

Welcome to Viewpoint, the new platform that replaces Inform. Once you have viewed this piece of content, to ensure you can access the content most relevant to you, please confirm your territory.

Viewpoint allows you to save up to 25 favorites.

Consider removing one of your current favorites in order to to add a new one.

Are you sure you would like to remove this page from your list?

Please sign in to set this content as a favorite., license content availability.

- Available Unavailable {{license}}

Stay signed in

Are you still working? Click here to extend your session to continue reading our licensed content, if not, you will be automatically logged off.

Hello and welcome to Viewpoint

Your go-to resource for timely and relevant accounting, auditing, reporting and business insights. Follow along as we demonstrate how to use the site

Before we start.

Choose your preferred language below.

Home » Blog » Restatement of Financial Statements and their Disclosure as per Ind AS 8

Restatement of Financial Statements and their Disclosure as per Ind AS 8

- Blog | News | Account & Audit |

- Last Updated on 28 May, 2022

Recent Posts

Blog, News, GST & Customs

Bail Granted Due to Investigation Lapses in Issuing Fake Invoices Under GST | HC

Blog, News, Insolvency and Bankruptcy Code

Delisting of Equity Shares Under Approved Resolution Plan Would Be Governed by IBC; Overrides SEBI Delisting Norms | HC

Latest from taxmann.

Where the financial statements of an enterprise contain either material errors or immaterial errors made intentionally or unintentionally to achieve a particular presentation of an entity’s financial position, financial performance, or cash flows, then the said financial statements are considered to be in non-compliance with Ind ASs. It may happen that the potential current period errors discovered in a particular period are corrected before the financial statements are approved for issue. But in some cases, material errors are left undiscovered until a subsequent period. Such prior period errors, when discovered, are corrected in the year of discovery, by adhering to the principles as prescribed in Ind AS 8, Accounting Policies, Changes in Accounting Estimates and Errors, as below:

Para 42 states that an entity shall correct material prior period errors retrospectively in the first set of financial statements approved for issue after their discovery by:

( a ) restating the comparative amounts for the prior period( s ) presented in which the error occurred; or

( b ) if the error occurred before the earliest prior period presented, restating the opening balances of assets, liabilities, and equity for the earliest prior period presented.

For Example, While preparing the financial statements for the year 2021-22 (current year), if any material error is discovered for the year 2018-19 (the year before the earliest prior period), then the financial statements of the entity is corrected by restating the opening balances of relevant assets and liabilities & relevant component of equity for the year 2020-21( earliest prior period). This will result in a consequential restatement of opening balances for the year 2021-22.

However where it is impracticable to determine either the period-specific effects, the cumulative effect of the error, or the amount of an error, then an entity shall :

(a) In case of the period-specific effects of an error is impracticable to determine, the entity shall restate the opening balances of assets, liabilities, and equity for the earliest period for which retrospective restatement is practicable (which may be the current period).

(b) In case the cumulative effect of an error is impracticable to determine, at the beginning of the current period, of an error in all prior periods, the entity shall restate the comparative information to correct the error prospectively from the earliest date practicable.

(c) In case the amount of an error for all prior periods is impracticable to determine, the entity shall restate the comparative information prospectively from the earliest date practicable

Ind AS 8 further states that the correction of a prior period error is excluded from profit or loss for the period in which the error is discovered. Any information presented about prior periods, including any historical summaries of financial data, shall be restated as far back as is practicable.

Disclaimer: The content/information published on the website is only for general information of the user and shall not be construed as legal advice. While the Taxmann has exercised reasonable efforts to ensure the veracity of information/content published, Taxmann shall be under no liability in any manner whatsoever for incorrect information, if any.

Taxmann Publications has a dedicated in-house Research & Editorial Team. This team consists of a team of Chartered Accountants, Company Secretaries, and Lawyers. This team works under the guidance and supervision of editor-in-chief Mr Rakesh Bhargava.

The Research and Editorial Team is responsible for developing reliable and accurate content for the readers. The team follows the six-sigma approach to achieve the benchmark of zero error in its publications and research platforms. The team ensures that the following publication guidelines are thoroughly followed while developing the content:

- The statutory material is obtained only from the authorized and reliable sources

- All the latest developments in the judicial and legislative fields are covered

- Prepare the analytical write-ups on current, controversial, and important issues to help the readers to understand the concept and its implications

- Every content published by Taxmann is complete, accurate and lucid

- All evidence-based statements are supported with proper reference to Section, Circular No., Notification No. or citations

- The golden rules of grammar, style and consistency are thoroughly followed

- Font and size that’s easy to read and remain consistent across all imprint and digital publications are applied

Leave a Reply Cancel reply

Your email address will not be published. Required fields are marked *

Save my name, email, and website in this browser for the next time I comment.

PREVIOUS POST

To subscribe to our weekly newsletter please log in/register on Taxmann.com

Latest books.

Commentary Combo-II for-Direct Taxes

Commentary Combo-I for Direct Taxes

Essentials Combo Direct Taxes

Income Tax Rules

Everything on Tax and Corporate Laws of India

Author: Taxmann

- Font and size that's easy to read and remain consistent across all imprint and digital publications are applied

Everything you need on Tax & Corporate Laws. Authentic Databases, Books, Journals, Practice Modules, Exam Platforms, and More.

- Express Delivery | Secured Payment

- Free Shipping in India on order(s) above ₹500

- +91 9910274007

- Academic Publications

- Professional – Law & Taxation Publications

- Subscriptions & Online Resources

- Training & Professional Courses

- Company Pages

- Media Coverage

- Company Offerings

- Budget Pages

- Union Budget 2024-25

- Company Policies

- Privacy Policy

- Return Policy

- Payment Terms

- Business & Support

- Sell with Taxmann

- Locate Dealers

- Locate Representatives

3.7 Restatements and Corrections of Accounting Errors

3.7.1 identifying accounting errors, 3.7.2 evaluating accounting errors.

- “Financial statements or specific line items . . . are irrelevant to investors’ investment decisions.”

- Errors in previously issued financial statements are not material because other registrants also made the error.

- One error is not material because it is offset by another error.

3.7.3 Corrective Action

- “The cumulative effect of the error on periods prior to those presented shall be reflected in the carrying amounts of assets and liabilities as of the beginning of the first period presented.”

- “An offsetting adjustment, if any, shall be made to the opening balance of retained earnings (or other appropriate components of equity or net assets in the statement of financial position) for that period.”

- “Financial statements for each individual prior period presented shall be adjusted to reflect correction of the period-specific effects of the error.”

- Inclusion, in the auditor’s report, of an additional paragraph referring to the restatement.

- Individual financial statements labeled “as restated.”

- Disclosures in the financial statements in accordance with ASC 250.

- Financial statement column headings do not have to be labeled “as restated.”

- An additional paragraph in the auditor’s report is typically not necessary.

3.7.4 Impact on Internal Control

- “A deficiency in [ICFR] exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent or detect misstatements on a timely basis.”

- “A significant deficiency is a deficiency, or a combination of deficiencies, in [ICFR] that is less severe than a material weakness, yet important enough to merit attention by those responsible for oversight of the company’s financial reporting.”

- “A material weakness is a deficiency, or a combination of deficiencies, in [ICFR], such that there is a reasonable possibility that a material misstatement of the company’s annual or interim financial statements will not be prevented or detected on a timely basis.”

3.7.5 Additional IPO Considerations

- As stated in Section 1.4.1 , depending on the length of time between amendments, financial statements and other information included in the registration statement may need to be updated to reflect subsequent periods. Such an update may include adding an additional year of audited financial statements. In some cases, an error or errors may be identified during the audit for the subsequent year (or years). Depending on the materiality of the error(s), figures may be restated after the initial registration statement has been submitted to the SEC. Once the effects of a correction of an error on prior periods have been disclosed in issued annual financial statements, disclosure of the restatement does not need to be repeated when the restated amounts are presented as prior-period comparative amounts in subsequently issued annual financial statements. In this context, interim financial information is not considered the equivalent of issued annual financial statements. In addition, the reissuance of financial statements that do not include any additional annual periods (e.g., a subsequent registration statement amendment that does not yet include an additional annual period of audited financial statements) does not meet this requirement, and the “as restated” or similar language should be retained to identify the period(s) restated. The restatement language may be removed once the subsequent issuance of annual audited financial statements is completed.

- Restatements can prolong the registration process because each amendment can result in additional SEC comments.

- CEOs and CFOs of newly public companies are subject to certain provisions of Sarbanes-Oxley and Dodd-Frank that may compel them to disgorge bonuses or other compensation earned during periods for which related financial information is subsequently restated. Specifically, under Section 304 of Sarbanes-Oxley, CEOs and CFOs may be required to return compensation received within the 12-month period following the public release of financial information if there is a restatement of such financial information because of material noncompliance, due to misconduct, with financial reporting requirements under the federal securities laws.

- Executive officers, including the CEO and CFO, of newly public companies listed on national exchanges will be subject to expanded executive compensation clawback policies as well. In October 2022, the SEC issued a final rule to implement the Section 954 mandate of Dodd-Frank to ensure that executive officers do not receive “excess compensation” if the financial results on which previous awards of compensation were based are subsequently restated because of material noncompliance with financial reporting requirements. Such restatements would include those correcting an error that either (1) “is material to the previously issued financial statements” (a “Big R” restatement) or (2) “would result in a material misstatement if the errors were corrected in or left uncorrected in the current report” (a “little r” restatement). Specifically, the final rule requires issuers to “claw back” excess compensation for the three fiscal years before the determination of a restatement regardless of whether an executive officer had any involvement in the restatement. The final rule also requires an issuer to disclose its recovery policy in an exhibit to its annual report and to include new checkboxes on the cover page of its annual report to indicate whether the financial statements “reflect correction of an error to previously issued financial statements and whether [such] corrections are restatements that required a recovery analysis.” Additional disclosures are required in the proxy statement or annual report when a clawback occurs. Such disclosures include the date of the restatement, the amount of excess compensation to be clawed back, and any amounts outstanding that have not yet been clawed back. Companies undertaking an IPO are required to adopt a clawback policy that complies with the requirements before being listed on a national exchange. However, compensation received before the company is listed on a national exchange does not have to be clawed back under the SEC rule. For further details on the final rule, see Deloitte’s November 14, 2022, Heads Up .

Impact and Process of Financial Statement Restatements

Explore the structured approach to correcting financial statements, including the roles of auditors and communication strategies.

Financial statement restatements are significant events in the corporate world, often triggering a meticulous review of past financial records and practices. These adjustments are necessary to correct inaccuracies in previously issued financial statements, which can stem from unintentional errors to deliberate fraud. The implications of such restatements are broad, affecting everything from investor confidence to regulatory scrutiny.

Understanding why these restatements occur and how they are handled is crucial for stakeholders ranging from investors to company executives. This process not only seeks to rectify past information but also aims to reinforce future financial reporting’s transparency and accuracy.

Reasons for Restating Financial Statements

Financial statements may need to be restated for a variety of reasons, each of which reflects different underlying issues within a company’s financial reporting processes. These reasons can range from simple mathematical errors to complex legal issues, and understanding them is essential for comprehending the impact of restatements.

Error Corrections

Errors that necessitate the restatement of financial statements can arise from a multitude of oversights such as mathematical mistakes, misapplication of accounting principles, or oversight of certain transactions. For instance, in 2015, Toshiba restated its profits after it was found that there had been prolonged accounting errors, overstating its pre-tax profits by nearly $1.2 billion over seven years. Such corrections are typically identified during internal audits or through external audit feedback. The process of correcting these errors involves a detailed review of all past financial documents to ensure the accuracy and integrity of financial reporting.

Fraudulent Activities

Financial restatements due to fraudulent activities involve intentional misrepresentations made by company officials to deceive stakeholders. A high-profile example is the Enron scandal, where the energy giant’s collapse in 2001 was precipitated by the revelation of systematic accounting fraud, leading to significant restatements of its financial statements. These activities can include manipulation of financial records, omission of significant information, or misuse of funds. Detecting fraud usually requires forensic accounting techniques and can lead to legal actions, besides the financial restatement itself.

Changes in Accounting Policies

Sometimes, restatements are necessitated by changes in accounting policies or regulations. When accounting standards are updated, companies may need to alter their financial reporting to comply with the new requirements. For example, the transition from Generally Accepted Accounting Principles (GAAP) to International Financial Reporting Standards (IFRS) has led to restatements for numerous companies to align with global accounting standards. This type of restatement ensures that financial statements provide a true and fair view under the current accounting framework and maintain comparability with other entities following the same standards.

Steps in the Restatement Process

Once the need for a restatement is identified, a structured process is initiated to ensure that the revised financial statements accurately reflect the company’s financial status. This process involves several critical steps, from the initial identification of discrepancies to the final approval and dissemination of corrected financial data.

Identification of Errors or Misstatements

The first step in the restatement process is the identification of errors or misstatements. This typically begins with a signal or suspicion, which could arise from an internal audit, whistleblower activity, or regulatory review. Once a potential issue is flagged, a thorough examination of relevant financial records is conducted. This examination might involve revisiting transaction logs, audit trails, and communication records to pinpoint the origin and extent of the error. The goal is to gather enough evidence to accurately assess the impact of the misstatement on previous financial reports.

Calculation of Adjustments

After identifying the specific errors or misstatements, the next step involves calculating the necessary adjustments to correct the financial statements. This task requires a detailed analysis of the financial impacts over the affected periods. Financial analysts and accountants work together to quantify the adjustments needed, ensuring they reflect the true financial position of the company. This might involve recalculating financial ratios, revising balance sheets, and altering income statements to correct the inaccuracies previously reported. The accuracy of these calculations is paramount to restore trust and maintain regulatory compliance.

Approval and Documentation Process

The final step in the restatement process is obtaining approval for the adjustments and properly documenting the changes. This phase often involves several layers of internal and external approval to ensure the restatement meets all regulatory and legal standards. The company’s board of directors, along with independent auditors, typically reviews and approves the restated financial statements. Comprehensive documentation is also crucial, as it provides a transparent record of the errors, the adjustments made, and the approval process. This documentation is essential not only for regulatory compliance but also for maintaining historical accuracy and providing clarity to stakeholders.

Role of Auditors in the Restatement Process

Auditors play a multifaceted role in the restatement process, often serving as both detectives and advisors. Their primary function is to provide an independent assessment of the company’s financial statements, ensuring that any restated figures are accurate and in accordance with applicable accounting standards. When a restatement is necessary, auditors delve into the company’s financial records to validate the scope and accuracy of the reported figures. They scrutinize the adjustments proposed by the company to ensure that they correct the misstatements without introducing new errors.

Beyond verification, auditors also offer guidance on the implementation of improved controls and processes to prevent future misstatements. They evaluate the company’s internal controls and may recommend enhancements to reduce the risk of inaccuracies in financial reporting. This advisory role is crucial as it helps companies to not only address the immediate issues that led to the restatement but also to fortify their financial reporting framework against potential future errors.

Auditors’ involvement continues with the monitoring of the restatement’s aftermath. They observe the company’s adherence to the revised practices and controls, ensuring that the changes made are effective and sustainable. This ongoing oversight helps to rebuild stakeholder confidence in the company’s financial integrity and reporting practices.

Communicating Restatements to Stakeholders

When a company faces the necessity of restating its financial statements, transparent and effective communication with stakeholders is paramount. This process begins with a clear, concise announcement that not only acknowledges the restatement but also explains the reasons behind it. It is important for the company to maintain an open line of communication to mitigate any potential uncertainty or negative perceptions. Stakeholders, including investors, employees, and customers, should receive timely updates as the restatement process unfolds. This approach helps in maintaining trust and demonstrates the company’s commitment to transparency and ethical practices.

The communication strategy should also include detailed explanations of the impacts of the restatement on the company’s financial health and operations. This might involve hosting webinars or conference calls where executives and financial officers can discuss the restatement’s implications and field questions from stakeholders. Providing a forum for dialogue reassures stakeholders of the company’s handle on the situation and its strategies for moving forward.

Managing Conflicts of Interest in Accounting

Maintaining ethical standards in accounting, you may also be interested in..., managing cognitive and affective conflict in teams, mercantile law: principles, contracts, and modern developments, understanding shareholders: roles, rights, and impact on corporate governance, strategies for efficient audit time budget allocation.

Restatements: the costly result of an error

Jul 26, 2019 · Authored by

Corporate officers, auditors and audit committees all work towards ensuring US publicly traded companies provide accurate corporate financial reports to investors. However, even with all of the different components working diligently to present clear and accurate reports, errors do occur. How the error is rectified depends on the timing and severity of the offense.

In some cases, the error is alleviated through a restatement. While innocent sounding, a restatement can be devastating. Thus, it is important to understand when they are necessary, how it can affect you, and how to avoid the situation altogether.

What is a restatement of a financial statement?

The Financial Accounting Standards Board (FASB) defines a restatement as a revision of a previously issued financial statement to correct an error. Restatements are required when it is determined that a previous statement contains “material” inaccuracy. However, FASB offers minimal guidance in defining materiality. Accountants are responsible for determining whether a past error is “material” enough to need a restatement. The Securities and Exchange Commission (SEC) suggests companies and auditors conduct quantitative and qualitative analysis to identify any errors in prior financial statements.

Often, “material” inaccuracies stem from accounting mistakes, noncompliance with generally accepted accounting principles (GAAP) or other frameworks, fraud, misrepresentation or clerical errors.

In what instances are restatement filed?

A “material” error affecting part or all of a financial statement often triggers a restatement.

Typically, these errors are a result of innocent mistakes and/or basic misinterpretation. Some leading causes for restatements include:

- Recognition errors – For example, when accounting for leases or reporting compensation expense from backdated stock options.

- Income statement and balance sheet misclassification – For instance, a company may need to shift cash flows between investing, financing and operating on the statement of cash flows.

- Mistakes reporting equity transactions – This includes improper accounting for business combinations and convertible securities.

- Valuation errors related to common stock issuances

- Preferred stock errors

- Complex rules related to acquisitions, investments, revenue recognition and tax accounting

In addition, companies often issue restatements when their financial statements are subjected to an elevated degree of scrutiny. For example, restatements occur when a private company converts from compiled financial statements to audited financial statements or decides to file for an initial public offering (IPO). Other cases of restatements include when an owner elects to utilize additional internal (or external) accounting expertise, such as a new controller or audit firm.

The Molson Coors Brewing Co. Case

No company, regardless of their size, is given a pass for accounting errors – whether those mistakes are innocent or malicious. The announcements can be very public and the effects can hinder even the most robust companies.

In February 2019, Molson Coors Brewing Co. (brands include Coors Light, Blue Moon, and Killian’s Irish Red) revealed it was issuing restatements for fiscal years 2016 and 2017 . The restatements came after auditors discovered accounting errors for income taxes related to deferred tax liabilities.

Their explanation filed with regulators placed the blame on the acquisition of the remaining 58% stake of MillerCoors in 2016. By understating deferred tax liability and income tax expense, the net profits ballooned by nearly $400 million in 2016. Overall, Molson Coors claims the understated value of the taxes owed, but not yet paid on its balance sheet, amounted to $248 million. Their equity was overstated by the same amount.

Company shares fell by 6.4% following the restatement announcement.

What are the restatement requirements?

In the event that a publicly held company must file a restatement it takes two main steps:

- File a Form 8-K to notify the investment community.

- Issue replacement Forms 10-Q and 10-K, as applicable.

Companies must file SEC Form 8-K within four days in order to alert investors of “non-reliance” on the previously issued financial statements.

Amended Form 10-Q is required for affected quarters, and Form 10-Ks are necessary depending on how many prior periods are affected.

How does the SEC factor in?

It is the primary focus of the SEC to ensure US companies are presenting accurate information to investors and other stakeholders. As such, the SEC reviews public companies, and some private ones, to verify no violations of security laws have occurred and the companies have complied with financial reporting standards. These more thorough reviews typically take place following press releases, media reports, anonymous tips or amended filings of periodic reports.

More specifically, the SEC may initiate a formal investigation into a potential restatement or fraud case. This decision hinges on factors such as available resources, potential discoveries of misstatements, company-specific characteristics and relevance on emerging accounting and financial reporting matters.

In fact, the SEC’s Enforcement Division instituted a Financial Reporting and Audit (FRAud) Group as part of their efforts to identify and prosecute securities law violations related to reporting and audit failures. The FRAud Group is specifically focused on identifying and exploring areas susceptible to fraudulent financial reporting. These dedicated efforts include an ongoing review of financial statement restatements and revisions.

What happens when the SEC steps in?

When restatements are announced, it can shake investor confidence in the company. However, when the SEC takes action, it can be costly and devastating.

For example, in early January 2019 the SEC imposed a $16 million civil penalty on Hertz Global Holdings and their rental car subsidiary, Hertz Corporation, for misstating pretax income as a result of accounting blunders . According to the SEC, the company’s public financial filings “materially misstated” pretax income due to errors in a number of business units, particularly in areas subject to management estimates.

Subsequently in February 2019, Kraft Heinz revealed they received an SEC subpoena in October 2018 as part of an investigation into their accounting and procurement policies. The company claimed to launch an internal investigation into the matter. Following the conclusion of their investigation, the company posted a $25 million increase to the cost of products sold after determining it was “immaterial to the fourth quarter of 2018 and its previously reported 2018 and 2017 interim and year to date periods.” Kraft Heinz explained they were cooperating fully with the SEC subpoena. They also announced efforts to improve internal controls and procedures to prevent future mishaps. Upon the subpoena disclosure, shares in the company crumbled by nearly 25% in futures trading.

Later, in May 2019, Kraft Heinz announced the restatement of three years’ worth of financial reports following their investigation.

They acknowledged that the errors resulted from lapses in procurement procedures by some employees. In the same announcement, the company revealed they received an additional subpoena from the SEC related to the assessment of goodwill and asset impairments. The subpoena also called for the documents regarding procurement operations.

There are two major takeaways from these very recent cautionary tales:

- The SEC will take severe civil action against inaccurate financial statements.

- Once the SEC discovers some errors in accounting procedures, they will continue to dig deeper and deeper into your policies. Even if they do not exact penalties, the effects can be felt in the stock market.

What preventative steps can I take to avoid a restatement?

It is in the best interest of companies to take the necessary precautionary steps to avoid future restatements. Seeing as restatements are public admissions of unreliable financial statements, a common outcome following a restatement is a sudden decline in the stock price of an organization. In fact, the American Institute of Certified Public Accountants (AICPA) specifically lists “restatement of previously issued financial statements to reflect the correction of a material misstatement due to fraud or error” as an indicator of material weaknesses in internal controls.

So what can you do to avoid a restatement and maintain investor confidence?

- First and foremost, preventing financial restatements begins with an ongoing identification of potentially susceptible areas of your financial reporting processes. Management and other senior leadership should lend particular scrutiny to financial reporting steps involving complex accounting standards, significant use of estimates, and recently issued accounting standards.

- Implementation of controls designed to mitigate risks. Upon integrating these controls, it is critical to monitor their effectiveness over time.

- Consider qualitative factors, in conjunction with quantitative ones, throughout decision making processes involving significant estimates or matters of judgment.

- Maintain timely awareness of evolving accounting standards, as well as new standards, and how they affect your company’s financial reporting. Allocate sufficient and proper resources necessary to ensure the accounting standards are properly applied.

Reporting your financial statements is a standard procedure for you and your company. It is vital to make sure you are exercising extensive awareness about your internal controls and ensuring the information reflected in those statements is accurate.

For more information on this topic or to learn how Baker Tilly specialists can help, contact our team .

Related sections

Sell-side advisory to a beer distributor.

- Search Search Please fill out this field.

What Is a Restatement?

Understanding restatements, the dangers of restatements, real-life example of a restatement, restatement requirements, special considerations, restatement faqs, the bottom line.

- Corporate Finance

- Financial statements: Balance, income, cash flow, and equity

Restatement: Definition in Accounting, Legal Requirements, Example

Daniel Liberto is a journalist with over 10 years of experience working with publications such as the Financial Times, The Independent, and Investors Chronicle.

:max_bytes(150000):strip_icc():format(webp)/daniel_liberto-5bfc2715c9e77c0051432901.jpg "presentation of restatement of financial statements")

Investopedia / Jake Shi

A restatement is an act of revising one or more of a company’s previous financial statements to correct an error. Restatements are necessary when it is determined that a previous statement contained a "material" inaccuracy. This can result from accounting mistakes, noncompliance with generally accepted accounting principles (GAAP), fraud, misrepresentation, or a simple clerical error.

Key Takeaways

- A restatement is a revision of one or more of a company’s previous financial statements to correct an error.

- Accountants are responsible for deciding whether a past error is “material” enough to warrant a restatement.

- An error can be considered material if the incorrect information would lead those receiving the statements to come to inaccurate conclusions.

- The FASB requires companies to issue a restatement to correct previously recorded errors.

- A reclassification involves correcting the classification of an entry.

Company management and independent auditors are responsible for ensuring that quarterly and annual financial statements accurately reflect the financial condition of a firm. Sometimes, previous statements need to be amended. At times, these mistakes will be spotted by internal auditors. On other occasions, it might be a third party, such as the Securities and Exchange Commission (SEC), that spots them.

The Financial Accounting Standards Board (FASB) requires companies to issue a restatement to correct previous errors. Accountants are responsible for deciding whether a past error is “material” enough to warrant a restatement.

Material is a loose term that is not accompanied by specific percentage guidelines and so forth. As a general rule of thumb, an error can be considered material if the incorrect information would lead those receiving the statements to come to inaccurate conclusions as part of a standard analysis.

If an issue or error is found that affects part of a financial document or the document as a whole, a restatement will likely be required. Additionally, if certain key information about the original statement is received after the first statement was released, a restatement may be issued to adjust the financials based on the discoveries.

Many restatements are the result of innocent mistakes and basic misinterpretation. However, some can raise red flags, highlighting potential fraud or incompetence. Over-reporting a company’s gains can be very misleading. It can lead investors to believe the company is in a stronger financial position than is actually the case. Based on the inaccurate information, investors may perform actions, in regards to the previously made investments, that otherwise would not have been made.

Public companies must file SEC Form 8-K to alert the investment community of material changes, as well as reissue corrected financial statements.

Negative restatements are regularly frowned on, shaking investor confidence and causing share prices to decline. They can also lead to fines: Hertz Global Holdings Inc. ( HTZ ) was ordered to pay a $16 million civil penalty after internal auditors discovered errors in several of its previous financial statements. In 2015, the car rental company disclosed that restatements would weigh on profits for 2011, 2012, and 2013.

In February 2019, Molson Coors Brewing Co. ( TAP ) revealed it would restate its financial statements for fiscal years (FY) 2016 and 2017 after auditors discovered accounting blunders for income taxes related to deferred tax liabilities (DTL).

In a filing with regulators, the beer maker blamed the errors on its acquisition of a remaining 58 percent stake in MillerCoors in 2016. Understating deferred tax liability (DTL) and income tax expense boosted net profits by nearly $400 million in 2016. Overall, the company said it understated the value of the taxes owed but not yet paid on its balance sheet by $248m, and overstated its total equity by the same amount.

The finding did not inspire much confidence in Molson Coors Brewing’s accounting practices, as reflected by the sharp subsequent markdown in the company’s share price.

When a publicly traded company determines it needs to amend its financial statements, it must file SEC Form 8-K within four days to notify investors of non-reliance on previously issued financial statements. It also needs to file amended 10-Q forms for the affected quarters and possibly amended 10-Ks , depending on how many accounting periods are affected by the erroneous data.

Companies should also provide a breakdown of how past errors occurred, how they were corrected, and whether there will likely be any future ramifications in their latest financial statements. These comments usually appear in the footnotes .

When companies issue restatements, investors are advised to ascertain to the best of their abilities the seriousness of the error reported. How much of an impact is it likely to have and, more importantly, was it an innocent mistake, or something that appears to be more sinister? Look for indications from management on how it plans to stop similar mistakes from happening in the future.

It is also worth remembering that changes in certain financial estimates are not required, as these are based on anticipated events and not ones that have already occurred. These changes must only be reported on the next financial statement after the change is made and are not applied retroactively.

What Is the Difference Between Reclassification and Restatement?

A restatement is the restatement of a revised financial statement. The restatement is purposed to correct what was previously reported erroneously. A reclassification involves correcting the classification of a transaction or entry, moving it from one ledger to another. For example, one could reclassify an entry from a current asset to a long-term asset.

What Is the Difference Between Revision and Restatement?

A revision is the correction of a reported amount in subsequent financial statements. However, the previously reported financial statement need not be reissued. With a restatement, on the other hand, the error must be material, prompting a revision and the issuance of a corrected financial statement.

What Is the Restatement of Torts?

The Restatement of Torts is a resource published by the American Law Institute (ALI) explaining the law as it pertains to certain situations, specifically involving torts. There are two Restatement of Torts: Restatement of the Law Second, Torts, and Restatement of the Law Third, Torts, which is the most recent published version.

What Is the Restatement of Contracts?

The Restatement of Contracts is a resource published by the American Law Institute (ALI) explaining the law as it pertains to contracts. In other words, they help courts clarify and interpret contract law.

When financial reports contain material inaccuracies, companies must correct the accounting error and reissue a corrected version of the financial statement. The error could have resulted from oversight, simple mistakes, or something more sinister, such as fraud. Despite the underlying reason, errors can cause those examining the statements to make decisions based on inaccurate data.

Bakertilly. " Restatements: the costly result of an error ." Accessed May 30, 2021.

Calc Bench. " Are restatements and revisions the same thing? " Accessed May 30, 2021.

USC Gould School of Law. " Tort Law ." Accessed May 30, 2021.

Cornell Law School. " Restatement of the Law ." Accessed May 30, 2021.

:max_bytes(150000):strip_icc():format(webp)/GettyImages-592232681-da0ca73d27994f0085bc3bda0ce50c30.jpg "presentation of restatement of financial statements")

- Terms of Service

- Editorial Policy

- Privacy Policy

- Your Privacy Choices

Accounting Resources

- Career Guides

- Interview Prep Guides

- Free Practice Tests

- Excel Cheatsheets

💡 Expert-Led Sessions 📊 Build Financial Models ⏳ 60+ Hours Learning

Restatement

Publication Date :

06 Jan, 2022

Blog Author :

WallStreetMojo Team

Edited by :

Ashish Kumar Srivastav

Reviewed by :

Dheeraj Vaidya, CFA, FRM

Table Of Contents

Restatement Meaning

A restatement corrects inaccuracies in financial statements pertaining to past accounting periods. These inaccuracies are caused by accounting errors, inaccurate financial reporting, clerical mistakes, frauds, and non-adherence to GAAP or accounting standards.

Not all errors have the same impact. Material errors are those that affect the final reporting. These impact financial figures to the extent that it results in inaccurate analysis and comparison. Financial statements are restated to ensure that stakeholders get an accurate picture of the company's financials.

- A restatement is the amendment of financial statements pertaining to one or more previous accounting periods. It rectifies errors resulting from material misappropriation.

- Material errors include clerical faults, non-compliance with accounting standards, fraud, or inaccurate financial reporting.

- Restating a financial statement also arises when there are changes in the accounting standards, changes in GAAP, changes in the corporate structure, or changes in the type of reporting organization.

- Financial statements can be restated as a reissuance, revision, or out-of-period adjustment.

Restatement Explained

A restatement is changing something that has been declared previously. Financial statements are restated to report errors. Not all errors have the same impact. Material errors are those that affect the final reporting. These errors impact financial figures to the extent that it results in inaccurate analysis and comparison.

Although accounting managers are responsible for presenting the correct financial reports every year, it is the auditors' responsibility to find errors in them. Such misappropriations can be identified by the internal auditors or the external authorities.

The issuance of restated financial statements is necessary so that the stakeholders , investors, financiers, and creditors get the correct picture of a company.

Reasons to Restate a Financial Statement

GAAP highlights the following three major reasons for restatement:

- Accounting Error : This includes all accounting mistakes like recording errors, improper accounting methods , and lack of information. As a result, the financial statements have to be restated.

- Non-Compliance with GAAP : Statements that fail to meet the Generally Accepted Accounting Principles guideline or any other accounting standard require restatements.

- Fraud or Misrepresentation : If the company or its accounting personnel deliberately reported incorrect financial information in the previous years, restating becomes necessary.

If any of the above errors are found, it has to pass the materiality test. Materiality is decided on the basis of impact. An error is considered material if it affects the stakeholders in their decision-making. Therefore, all errors do not need restating.

In addition to significant errors, there are some other errors:

- Changes in GAAP : If accounting standards like GAAP put forth new accounting methods or rules applicable from the current accounting period, restarting is required. However, if applied retrospectively, such changes would impact prior statements as well. In order to facilitate comparison then, restatement becomes necessary.

- Changes of Reporting Entity : If there are changes to the corporate structure or ownership type of the business entity , the comparative statement of the previous years has to be restated. Restating is done only when there is a significant impact on financial reporting .

Types of Restatement

The errors found in the previous years' financial statements determine the type of restatement the company has to proceed with. These are explained below:

#1 - Non-Reliance Restatement

A reissuance or "Big R Restatement" is issued when there are mass errors found in statements pertaining to earlier periods. Mass errors render previous and current financial statements unreliable.

The company, therefore, must restate publicly by filing an 8K form—an audit opinion states the restatement. An audit opinion is a statement expressed by independent auditors to their client's financial statements as the result of auditors' examination.

#2 - Revision Restatement

The stealth or small r restatement is released when a consolidated material error is discovered in various financial statements pertaining to previous years. Since it cannot be rectified with a one-time adjustment, doing so will result in misrepresentation of the current period's financial statement. Therefore, the company has to restate prior financial statements. This has to be mentioned in the footnotes of the current statements.

#3 - Out of Period Adjustments

If the degree of error is not significant enough to affect the reliability of any period's financial statement, then it doesn't require any restatement. However, its effect can be taken collectively and incorporated into the current financial statement. This should be accompanied by a disclosure note since it will affect the comparability.

Effect and Prevention

Every company should know the consequences of restating and ways to avoid one. Following are the effects of restating:

- If restatement is issued because of integrity or operational issues, the stakeholder's confidence in the company shatters.

- It generally results in excessive audit fees. The auditor has to dig into the errors and determine the type of restatement required for the particular case—it consumes a lot of time and effort.

- It furthers hampers the goodwill and credibility of the company since the investors, shareholders, and other associated parties lose trust in the firm's accounting system .

- Moreover, it undermines the company's valuation and thus limits funding.

Following are the ways of avoiding restatements:

- It is essential to conduct internal audits and accounts review before issuing the financial statement.

- Another crucial measure is to ensure a strong and effective internal control system to check misappropriation and fraud.

- Firms should address the accounting issues and the smallest error before it's too late. Firms must develop a culture of trust and transparency within the organization to eliminate chances of manipulation.

- It is equally important to have a team of expert accounting professionals who prepare accurate financial statements.

Restatement Example

Molson Coors Brewing Co. is a Chicago-based beverage company. They announced restated financial statements pertaining to 2016 and 2017. Molson's financial reporting bore material weakness related to deferred tax liabilities resulting in accounting error in its income tax computation. Therefore, under the guidance of its audit committee and Pricewater Coopers LLP, the firm decided to go for a non-reliance restatement of its financial statements.

Source - www.sec.gov

Frequently Asked Questions (FAQs)

Restating is the process of making amendments to the released financial statements pertaining to one or more previous accounting periods. This is done to rectify the material errors. The misrepresentation can be related to clerical mistakes, non-adherence to GAAP, accounting faults, and fraud.

A prior period adjustment refers to the rectifications made to the previous years' financial statements. It is a rectification of various accounting inaccuracies like wrong accounting methods, mathematical mistakes, or the ignoring of crucial information.

In accounting practice, any immaterial error can be corrected by revising the company's financial statements. This can be done for any of the previous three accounting periods. However, such rectification is permitted only once in every financial year. Also, the company has to seek permission from the respective Court of Audit. On the contrary, restatement corrects material inaccuracies in the previously issued financial statements (i.e., past accounting periods).

Recommended Articles

This article has been a guide to What is a Restatement & its Meaning. Here we discuss restatement types, examples, effects, and prevention. You can learn more about it from the following articles -

- Prior Period Adjustments

- Non Recurring Items

- Earnings Per Share (EPS)

- Steps in Accounting Process

IMAGES

COMMENTS

When the restatement is to be reflected in the soon-to-be issued comparative financial statements, the financial statements and auditor’s report would indicate that the prior periods have been restated. Users of the previously issued financial statements also must be notified that they should no longer rely on those financial statements.

Sep 17, 2024 · When the errors’ effect on the financial statements cannot be determined without a prolonged investigation (or the preparation, and auditing, of the restated financial statements will simply take a longer period of time due to the nature of the errors), the issuance of the restated financial statements and auditor’s report will necessarily ...

May 28, 2022 · Where the financial statements of an enterprise contain either material errors or immaterial errors made intentionally or unintentionally to achieve a particular presentation of an entity’s financial position, financial performance, or cash flows, then the said financial statements are considered to be in non-compliance with Ind ASs.

SAB Topic 1.M (codified in ASC 250-10-S99-1) indicates that “[i]n the context of a misstatement of a financial statement item,” while the relevant facts and circumstances include “the size in numerical or percentage terms of the misstatement, [they also include] the factual context in which the user of financial statements would view the ...

These filings include financial restatements when errors are discovered. Once the errors have been identified, prepare the restated financials, including disclosures within the restated financial statements regarding the reason for the misstatement, the impact to the financial statements, and the changes to internal controls.

May 4, 2024 · Once the need for a restatement is identified, a structured process is initiated to ensure that the revised financial statements accurately reflect the company’s financial status. This process involves several critical steps, from the initial identification of discrepancies to the final approval and dissemination of corrected financial data.

Jul 26, 2019 · For example, restatements occur when a private company converts from compiled financial statements to audited financial statements or decides to file for an initial public offering (IPO). Other cases of restatements include when an owner elects to utilize additional internal (or external) accounting expertise, such as a new controller or audit ...

Jul 27, 2021 · A restatement is the restatement of a revised financial statement. The restatement is purposed to correct what was previously reported erroneously. A reclassification involves correcting the ...

These impact financial figures to the extent that it results in inaccurate analysis and comparison. Financial statements are restated to ensure that stakeholders get an accurate picture of the company's financials. A restatement is the amendment of financial statements pertaining to one or more previous accounting periods.

to adapt the financial statement presentation of members’ or unitholders’ interests. Definitions 7 The following terms are used in this Standard with the meanings specified: General purpose financial statements (referred to as ‘financial statements’) are those intended to meet